Most technical guides explain what components exist in a remittance system. Almost none explain how those components actually talk to each other — the data flows, the backend processing layers, and the architecture decisions that determine whether your system handles ten transactions or ten million. This guide closes that gap entirely — giving you the complete remittance system architecture explained from the ground up, including system layers, data flow, and backend design.

What Is a Remittance System Architecture?

A remittance system architecture is the complete technical blueprint that governs how money moves from a sender in one country to a recipient in another. It encompasses every layer of software infrastructure — from the mobile interface a user touches to the settlement rails that finalize funds at a correspondent bank.

To understand how remittance systems are structured, it helps to think of the platform not as a single application but as a coordinated stack of specialised layers — each handling a distinct function within the transaction lifecycle. Unlike a standard payment system, a remittance system must simultaneously handle currency conversion, cross-border regulatory compliance, multi-rail routing, real-time fraud detection, and multi-currency settlement — all within a transaction lifecycle that can span minutes to days depending on the destination corridor.

Why Architecture matters?

The difference between a remittance platform that scales to millions of users and one that collapses under load is almost entirely architectural — not the product idea. System design determines latency, uptime, compliance readiness, and cost per transaction at scale. Understanding how remittance systems are built at the architectural level is the difference between a platform that scales and one that breaks.

Understanding remittance software systems at the architectural level means understanding how each layer is designed, what responsibilities it carries, and how data flows cleanly from one layer to the next without creating bottlenecks, compliance gaps, or settlement failures.

High-Level Architecture Overview:

At the highest level, a remittance system can be described as a six-layer stack, each layer serving a distinct function and communicating through well-defined interfaces. No single layer can operate independently — the system’s resilience is defined by how tightly these layers coordinate under load.

System Stack Framework:

Frontend → API Gateway → Backend Core → Payment Processing → Banking Integration → Compliance Engine

This six-layer model is the foundation of most modern money transfer system architectures. Each layer is independently scalable, which matters because compliance checks, for example, do not need to scale proportionally with the number of FX conversions happening simultaneously. Think of it as the remittance software architecture diagram explained in sequential form — each block representing a layer, each arrow representing a data handoff.

Core Layers of a Remittance System:

The following six layers constitute the full remittance software architecture. Together, these remittance system components define both the technical boundaries and the interaction model of the entire platform. Each is described here not only as a component definition, but in terms of its role within the larger system interaction model.

| Layer | Description | Role |

| Frontend Layer | Mobile apps, web portals, agent dashboards — user-facing interfaces that capture transaction intent | User-facing |

| API Layer | REST or GraphQL gateway that routes requests, enforces authentication, and translates data formats between frontend and backend | Gateway |

| Backend Layer | Microservices-based core: transaction engine, user management, FX rates service, ledger, and notification service | Core Logic |

| Payment Processing Layer | Handles card acquiring, bank debits, wallet top-ups, and FX conversion through a payment gateway — the financial engine of the transaction. | Financial |

| Banking Integration Layer | SWIFT, SEPA, ACH, local payment rails — connects the system to correspondent banks and payout networks globally. | Banking Rails |

| Compliance Layer | AML screening, KYC identity verification, sanctions list checks, and transaction monitoring runs in parallel with processing. | Regulatory |

Frontend Layer:

The frontend layer includes mobile applications (iOS and Android), web portals, and agent interfaces. Its architectural responsibility is minimal data handling — it captures user intent, validates input format, and passes structured requests to the API layer. A well-designed frontend layer stores no sensitive financial data locally and relies on the backend for all business logic.

API Layer:

The API layer is the system’s traffic controller. It authenticates incoming requests using OAuth 2.0 or JWT tokens, applies rate limiting to prevent abuse, and routes requests to the appropriate backend microservice. In a production-grade payment system architecture, the API layer is also where request logging begins — creating the audit trail that compliance will later depend on.

Backend Layer:

This is where the system’s intelligence lives. The backend layer runs as a collection of microservices — each owning a specific domain (transactions, users, FX rates, ledger entries) with no shared databases between services. This design prevents a failure in one service from cascading across the system.

Payment Processing Layer:

The payment processing layer interfaces with card networks, bank debit systems, and digital wallets to collect funds from the sender. It also runs the FX engine — pulling live exchange rates, applying margins, and locking in a rate for the duration of the transaction.

Banking Integration Layer:

This layer manages payout to the recipient’s bank or mobile wallet. It integrates with SWIFT for international bank wires, SEPA for euro-zone transfers, ACH for US domestic payouts, and local real-time payment rails (UPI, FPS, etc.) for domestic delivery in specific corridors.

Compliance Layer:

Running largely in parallel with transaction processing, the compliance layer performs KYC checks on sender identity, screens against global sanctions lists (OFAC, UN, EU), applies AML rules, and monitors for behavioral anomalies that might indicate fraud or money laundering. This layer must never become a bottleneck — it is typically designed with sub-200ms response time targets.

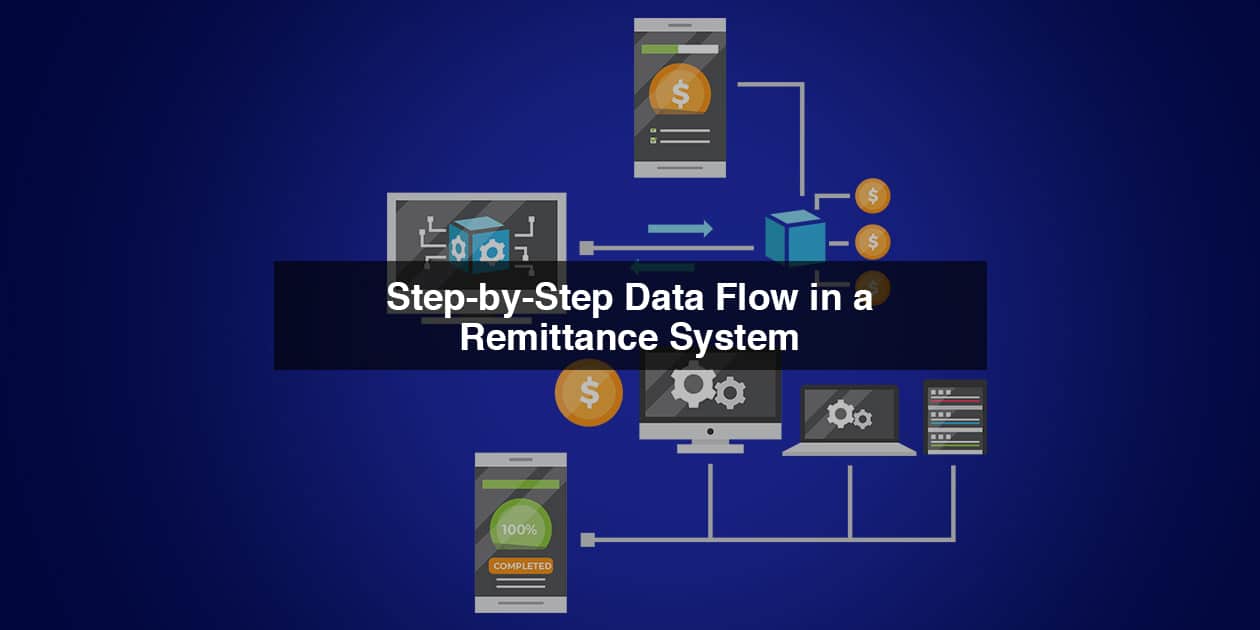

Step-by-Step Data Flow in a Remittance System

The following is the complete transaction path for a single remittance — from the moment a user initiates a transfer to the moment funds appear in the recipient’s account. This is the section that most remittance system workflow guides skip entirely.

1. User Initiates a Transfer

The sender enters recipient details, transfer amount, and destination country through the frontend. The frontend validates format, then packages the request and sends it to the API gateway via HTTPS. No processing occurs at this stage — only input capture.

2. Data Enters the System

The API gateway authenticates the session token, applies rate limiting, logs the raw request, and routes it to the Transaction Service in the backend. A unique transaction ID is generated and assigned at this point — this ID follows the transaction through every downstream system.

3. KYC Validation

The compliance engine runs KYC verification in parallel with the transaction setup. It checks the sender’s identity against stored KYC records and the transfer against daily and monthly limit rules. If the sender is new or the amount exceeds thresholds, the compliance engine may trigger an enhanced due diligence flow before allowing the transaction to proceed.

4. Payment Collection

Once compliance clears the transaction, the payment processing layer initiates a debit against the sender’s payment method — card charge, bank debit, or wallet deduction. The payment processor returns an authorization token, which is stored against the transaction record in the ledger service.

5. FX Conversion

The FX engine is invoked to convert the collected amount into the destination currency. Exchange rates are pre-fetched from liquidity providers and cached at the FX service layer. The locked rate, conversion amount, and fee breakdown are recorded on the transaction ledger entry before routing begins.

6. Routing Decision

The routing engine evaluates all available payout rails for the destination corridor — SWIFT, local bank rails, mobile money networks — and selects the optimal route based on cost, speed, and reliability parameters. Routing logic is configurable at the corridor level, not hardcoded, allowing real-time failover if a primary rail is degraded.

7. Settlement

The banking integration layer transmits the payment instruction to the correspondent bank or payout partner. For SWIFT transfers, a SWIFT MT103 message is generated. For local rails, the format varies by network. Settlement confirmation is received asynchronously and the transaction status is updated in the ledger when confirmation arrives.

8. Delivery Confirmation

Upon settlement confirmation, the notification service triggers SMS, email, and in-app alerts to both sender and recipient. The transaction is marked complete in the ledger, all audit records are finalized, and the transaction ID can now be used for post-delivery queries or dispute resolution.

Data Flow Framework: Input → Validation → Processing → Routing → Settlement → Output

Backend Architecture

The backend is where the heaviest architectural decisions are made. What distinguishes a robust payment system backend architecture from a brittle one is not the choice of language or framework — it is service isolation, event-driven communication, and idempotent operations. Modern remittance platforms use a microservices architecture rather than a monolithic application — for good reason.

| Service | Description |

| Transaction Engine | Integrate the full transaction lifecycle, create records, manage state transitions, coordinate microservice calls, and handles retries on failure. |

| Database Layer | Typically a combination of PostgreSQL for transactional data (ACID compliance required), Redis for session and rate caching, and time-series databases for FX rate history. |

| Notification Service | Asynchronous service that listens on an event bus for transaction state changes and dispatches SMS, email, push, and WhatsApp alerts at each milestone. |

| Ledger Service | Immutable, append-only record of all financial movements. Every debit, credit, fee, and FX conversion is recorded as a ledger entry with a timestamp and transaction ID. |

| FX Rate Engine | Fetches rates from multiple liquidity providers, applies configured margins per corridor, locks rates for open transactions, and publishes rate feed for the frontend quote display. |

| User Management Service | Manages user accounts, KYC status, document storage references, transaction limit profiles, and authentication tokens across the system. |

In a microservices setup, inter-service communication typically uses a message queue (Apache Kafka or RabbitMQ) for asynchronous events, and direct HTTP or gRPC calls for synchronous operations. This separation ensures that a spike in notification volume, for example, does not affect transaction processing speed.

Payment Integration Layer

The payment integration layer is where the remittance system connects to the external financial world. It is the layer most likely to introduce latency, and the one that requires the most careful error handling and retry logic.

For a complete view of cross-border payment systems, this layer must support multiple concurrent integration types:

- Card acquiring: Stripe, Adyen, or direct acquirer connections for Visa/Mastercard debit and credit card funding

- Bank debits: Open Banking APIs (PSD2 in Europe), ACH pull in the US, Faster Payments in the UK

- SWIFT messaging: MT103 for credit transfers, MT202 for cover payments in high-value corridors

- Local payment rails: UPI (India), PromptPay (Thailand), PIX (Brazil), BLIK (Poland), GCash (Philippines)

- Mobile money: M-Pesa, Orange Money, Airtel Money for payout in Sub-Saharan Africa

- Digital wallets: PayPal, Alipay, and WeChat Pay integrations for specific destination corridors

Architecture principle: Each payment rail integration should be implemented as an independent adapter behind a common interface. This means adding a new corridor or replacing a banking partner requires no changes to the transaction engine — only a new adapter implementation.

Compliance Layer

The compliance layer in a remittance system is not an afterthought — it is a core architectural component that must be designed from day one. The two primary compliance obligations in any AML and KYC systems context are Know Your Customer (KYC) and Anti-Money Laundering (AML).

| Component | Description |

| KYC Engine | Identity document verification (passport, national ID), facial recognition matching, proof-of-address validation, and ongoing monitoring of customer risk profile. |

| AML Screening | Real-time transaction monitoring against behavioural rules, sanctions list screening (OFAC, UN, EU, HMT), PEP checks, and adverse media monitoring. |

| Transaction Monitoring | Rule-based and ML-driven monitoring for velocity anomalies, structuring patterns, unusual corridor usage, and deviation from established customer behaviour profiles. |

| Regulatory Reporting | Automated generation of Suspicious Activity Reports (SARs), Currency Transaction Reports (CTRs), and other jurisdiction-specific regulatory filings. |

Architecturally, the compliance layer must be designed to run asynchronously where possible, with synchronous blocking only for high-risk checks (e.g., sanctions screening) that must resolve before a transaction proceeds. This hybrid approach is what allows compliant systems to achieve sub-second transaction acceptance times.

Scalability and Performance

A remittance system must be designed to scale horizontally from the start. Unlike e-commerce, where demand spikes are somewhat predictable, cross-border payment volumes can surge unpredictably during festivals, natural disasters, or geopolitical events that trigger mass fund transfers.

Key scalability principles that distinguish production-grade remittance software architecture from prototype-level systems include:

- Stateless services: Every microservice should be stateless so that instances can be added or removed without affecting in-flight transactions

- Event-driven design: Use Kafka or similar for inter-service communication, creating a natural buffer against load spikes

- Database read replicas: Route read-heavy queries (transaction status, balance checks) to read replicas to offload the primary write database

- Caching at multiple layers: FX rates, user session data, and KYC status should all be cached in Redis to reduce database round-trips

- Circuit breakers: If a downstream integration (bank API, compliance provider) degrades, circuit breakers prevent cascading failure across the system

- Idempotent transaction handling: All payment operations must be idempotent so that retries after network failure do not result in duplicate charges

Common Architecture Failures

Understanding failure modes is as important as understanding correct design. The following are the most common architectural mistakes in remittance system design — and why they matter at scale.

Monolithic Backend with No Service Isolation:

A single backend codebase means a compliance engine slowdown freezes transaction processing. Service isolation is non-negotiable for production systems — not an optimization for later.

Synchronous compliance blocking all transactions:

Running all AML and KYC checks synchronously in the transaction path creates a compliance bottleneck. Most checks should run in parallel, with only critical sanctions screening blocking the flow.

No idempotency on payment operations:

Without idempotency keys, a network timeout that causes a retry can result in a customer being charged twice. Every payment API call must include an idempotency key tied to the transaction ID.

Hardcoded routing logic per corridor:

Embedding routing rules in code instead of a configurable rules engine means that switching a banking partner for a single corridor requires a code deployment — a critical operational risk during an outage.

FX rates fetched per transaction:

Calling a liquidity provider API for every FX conversion introduces unnecessary latency and cost. Rates should be pre-fetched on a schedule and cached, with the cache invalidated when rate movement exceeds a threshold.

No audit log separation:

Storing audit records in the same database as transaction data creates a compliance risk — a database migration or data purge could delete regulatory records. Audit logs must be written to a separate, immutable store.

Frequently Asked Questions

1. What is the difference between remittance system architecture and payment system architecture?

Payment systems typically handle domestic, single-currency transactions between known parties. Remittance system architecture adds cross-border FX conversion, multi-rail international routing, global compliance requirements, and correspondent banking integrations All of which require additional architectural layers not present in a basic payment system.

2. What database is best for a remittance system?

Most production remittance platforms use PostgreSQL for transactional data (due to its ACID compliance and support for strong consistency), Redis for caching and session management, and an append-only ledger database (or a separate audit store) for financial records. Time-series databases are used for FX rate storage and monitoring metrics.

3.Should a remittance system use microservices or a monolith?

For production-scale remittance systems, microservices are strongly preferred — particularly because compliance, FX, and payment processing have very different scaling characteristics. A monolith can work for an MVP, but the refactoring cost later is significant. Systems expecting international operation from launch should begin with service boundaries in place, even if each ‘service’ is initially a module within a single deployment.

4. How does KYC fit into the transaction flow?

KYC is primarily a pre-transaction check. When a user registers, they undergo full KYC verification — identity document checks, facial matching, and address proof. At transaction time, the system checks the user’s KYC status and limit tier from the user management service. If the transaction exceeds the user’s verified limit, enhanced due diligence is triggered before the transaction proceeds.

5.What is the role of SWIFT in remittance system architecture?

SWIFT is a messaging network used to transmit payment instructions between correspondent banks. In remittance architecture, SWIFT is one of several rails in the banking integration layer — used primarily for high-value, bank-to-bank transfers where real-time local rails are not available. MT103 messages carry credit transfer instructions; MT202 messages are used for interbank cover payments.

backend

6.How do remittance systems handle failed transactions?

Failed transactions follow a structured exception path. The transaction engine catches the failure, logs the error state with a reason code, and triggers the notification service to alert the sender. Funds that were collected but could not be settled are automatically queued for refund processing. The ledger records both the failed debit and the reversal as separate entries to maintain an accurate audit trail.

7. How payment systems are designed differently from remittance systems, and how do money transfer systems work internally?

Payment systems are typically designed around a single currency, a domestic settlement rail, and a known counterparty relationship. Understanding how money transfer systems work internally reveals a more complex picture: remittance platforms must coordinate FX conversion, multi-rail routing, cross-border compliance, and correspondent banking relationships within a single transaction lifecycle. The result is a system with significantly more moving parts — and a much higher cost of architectural mistakes.

Conclusion

A production-grade remittance system architecture is not a single component — it is a coordinated six-layer system where every design decision has a downstream consequence. From the frontend that captures user intent to the compliance engine that screens every transaction in under 150ms, each layer must be built with clear boundaries, defined responsibilities, and the ability to scale independently.

What separates remittance platforms that survive growth from those that collapse under it comes down to a handful of non-negotiable architectural principles: microservices isolation in the backend, idempotent operations at the payment gateway layer, asynchronous AML and KYC compliance checks, configurable routing logic, and an immutable audit trail that sits entirely outside the transactional database.

Understanding how remittance systems are built — not just what components they contain, but how those components interact across a live transaction — is the foundation of every engineering and product decision you will make as you scale. Whether you are designing the payment system backend architecture from scratch or auditing an existing platform for failure points, the system relationships covered in this guide are where the real complexity lives.

The complete remittance system architecture is not a problem you solve once. It is an engineering discipline you maintain continuously — through load events, corridor expansions, regulatory changes, and banking partner failures. Build the layers right the first time, and the system handles everything else.